Source: ITSA

It may not have been like the in-person seminars we’re all accustomed to, or yearning for, but we were very happy to report that the International Tax Stamp Association (ITSA) webinar for the Latin American region, held on 3 December under the title ‘Illicit Tobacco during Lockdown: Controlling Tobacco in a COVID-19 Context’, drew close to 150 registrants from all over the Spanish-speaking world.

The attendees mainly comprised government representatives from tax, customs (and some health) authorities, including those in Chile, Colombia, Costa Rica, Ecuador, El Salvador, Haiti, Mexico, Nicaragua and Panama.

The webinar focused on the central role that traceability and tax stamps play in helping governments protect and recover the tax revenues they need right now, in this COVID world.

Juan Carlos Yáñez, current Chairman of ITSA, opened the webinar by stressing that one of the keys to an effective and competitively functioning tobacco market, as well as higher tax collection in times of COVID-19, was for governments to have an appropriate tobacco traceability system in place.

‘The need for strong fiscal returns has increased dramatically during COVID-19, as revenues have been seen to fall while government deficits and debt levels have been seen to increase accordingly’, said Juan Carlos during his welcome speech.

The global Illegal tobacco trade is estimated at upwards of $50 billion annually and totals more than 600 billion cigarettes, according to a 2020 World Bank report, causing negative impacts and impairing tobacco control measures implemented to protect public health.

Today, more than 90 countries around the globe use tax stamps to control illicit tobacco and/or alcoholic beverages. Many of these stamps combine the latest traceability technology with easily identifiable and highly secure product marking solutions, which is key to safeguarding revenues from tobacco, alcohol and other high tax goods.

The magnitude of the problem has made several countries in Latin America explore alternatives in line with the World Health Organisation Framework Convention on Tobacco Control (WHO FCTC) and its Protocol for the Elimination of Illicit Trade in Tobacco Products, said Juan Carlos.

Three speakers followed Juan Carlos’ introduction: Michel Jorratt, former director of the Chilean Tax Administration (Servicio de Impuestos Internos); Cédric Pruche, Director of Business Development for SICPA Mexico; and myself (Francisco Mandiola).

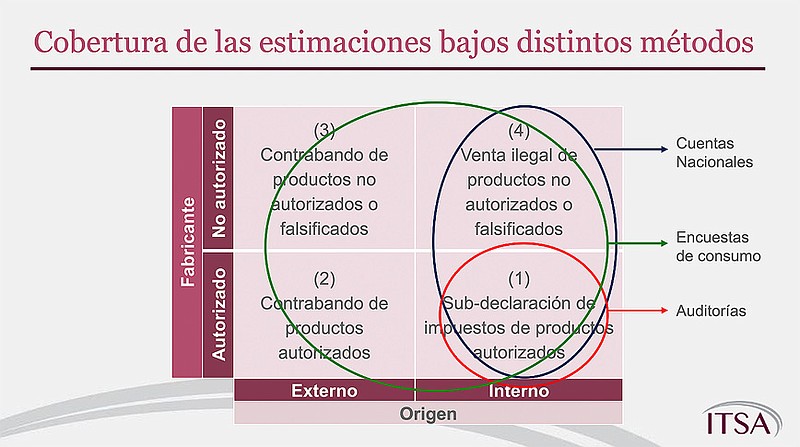

Michel Jorratt described a study he had conducted to evaluate the current level of tax evasion on tobacco products in Mexico and Chile, sharing the methodology used to calculate lost revenues as well as the estimated results for each country.

Michel started off by describing four different modes of tax evasion by manufacturers – both authorised and non-authorised and both in terms of local and internationally sourced products. These included cases where legally authorised tobacco manufacturers under-declared their production or sales levels. For each mode of tax evasion, he described the different methods and type of data used in their detection.

Michel stressed: ‘it is very difficult for tax authorities to effectively control the sale of illegal or contraband products without a good track and trace system’.

In Mexico’s case, the cigarette marking and traceability system in place since 2017 is linked to and operated by the tobacco industry in the country. In fact, Codentify, the system used, was originally designed and developed by Phillip Morris International to combat any attempt at effective government control of the tobacco industry.

Today, the Codentify solution is promoted by the company INEXTO, which has been hired directly by the tobacco industry to print the unique Codentify codes on the cigarette packs. The issue here, however, is that INEXTO has been hired without going through the compulsory certification process established by the Mexican Tax Administration Service (Servicio de Administración Tributaria).

Unpaid tax from tobacco in Mexico was estimated at close to $1 billion per annum and Michel’s analysis showed annual sales of close to 200 million illicit cigarettes – a clear sign that the existing system has, under the most lenient analysis, some flaws.

In the case of Chile, for the years 2011-2018, non-compliance with direct tobacco duties rose steadily from 17.3% to 25.6% in 2018. In addition, corporate taxes were also avoided by tobacco companies declaring lower overall yearly sales, presenting a dual problem for Chile’s tax authorities.

The Chilean Tax Administration (Servicio de Impuestos Internos) decided to launch an international public tender in 2018 in order to implement a modern tax stamp and traceability system and solve tax evasion issues. Among the bidders, two were offering the Codentify solution, and were disqualified because of their links with the tobacco industry, with the contract being finally awarded to an independent provider.

As a concluding remark, Michel described the importance of institutional coordination and the application of correct laws and sanctions for any new fiscal control system to function optimally.

My presentation focused on the importance of complying with the FCTC and Protocol from an ITSA viewpoint.

I reviewed the basic tenets of the FCTC as well as the importance of Article 8 of the Protocol, which specifically discusses track and trace systems and unique identification codes, but which does not specify the commercial or technological requirements for an ideal or immediate implementation, just general directives that don’t necessarily steer tax authorities in an optimal direction when analysing their tax stamp projects.

I then proceeded to explain the reasons behind ITSA’s writing and publication of its ‘Proposal for an FCTC Protocol-Compliant Tobacco Control System Blueprint’.

I detailed not only ITSA’s explicit recommendations but also my own opinion on best practice benchmarks worldwide, as well as the findings of The World Bank’s independent study with respect to how a country should implement a new and efficient tax stamp programme.

I further emphasised the importance of not only having a technically efficient tax stamp programme in place, but of also assuring that the nation’s laws and subsequent sanctions were in line with the tax authorities’ new requirements in order for the programme to be successful.

My presentation went into significant detail on the ITSA proposal, which can be read in its entirety at https://tax-stamps.org/proposal-for-an-fctc-protocol-compliant-tobacco-control-system-blue-print/.

I concluded with reasons as to why a correctly implemented tax stamp programme with an effective track and trace system independent from the tobacco industry would allow for:

Reduction in tax evasion/tax fraud.

Protection of the potentially dangerous effects of contraband.

Creation of a level and loyal competitive market.

Recovery of income for the government in a secure and verifiable manner.

Finally, Cédric Pruche’s presentation rounded up the webinar with an interesting mix of real cases from around the world where tax stamps have been successfully implemented.

Among the most interesting highlights of Cédric’s presentation was when he mentioned: ‘a well-planned tax stamp usually results in an increase of 20-50% in additional revenues for the state’.

Examples abound:

California increased revenues by $110 million upon launch of its tax stamps for cigarettes.

The SCORPIOS system in Brazil resulted in an increase in tax revenues of 24% and the closure of five illegal cigarette manufacturers after its first year in operation.

Ecuador successfully implemented the SIMAR system for tobacco, liquor and beer control in 2017 on 30 production lines in 17 factories, marking over 1 billion products per year. In a second step, the country is currently implementing aggregation for tobacco products which will allow the codes on each cigarette pack to be linked to their respective cartons, master cases and pallets to control logistics movements in compliance with Article 8 of the Protocol.

In Chile, the SITRAF TAB system was installed in 2019 and expects to significantly decrease the estimated $300 million in lost cigarette tax revenues.

In Dominican Republic, the TRAFICO system was implemented in early 2020 and has already increased tax revenues by $70-$85 million and reduced evasion by 6%-8%.

Cédric’s presentation concluded with a look at other products on which tax stamps/markers and traceability systems are – or could be – applied. These include all types of alcoholic beverages, cannabis products, gas and oil products and pharmaceuticals.

The webinar closed with a lively Q&A session from our attendees.

A recording of the entire one-hour session, in Spanish, is available on the ITSA website at https://tax-stamps.org/events/.