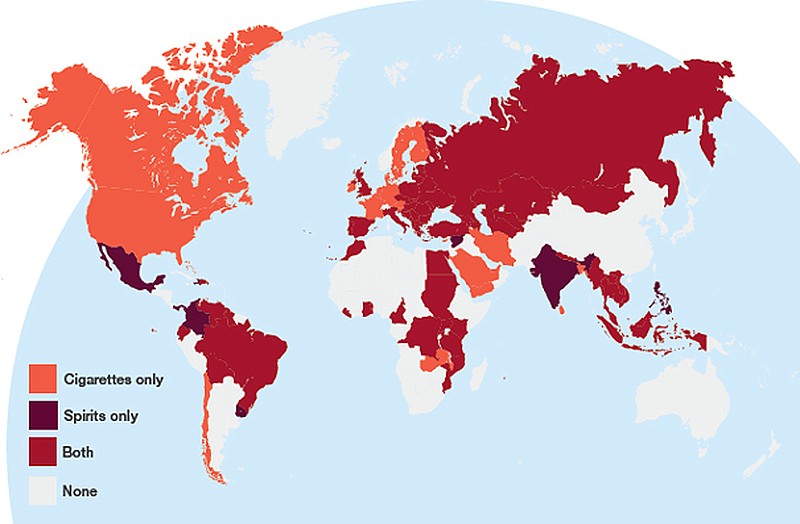

Fig 1 – global use of cigarette and spirits tax stamps.

A review by Ian Lancaster, project leader for ISO 22382 tax stamp guidance standard.

‘Tax stamps have a relatively young history, but a demonstrably successful one. They are likely to remain the weapon of choice for revenue authorities for a good number of years yet.’

That statement, which is the conclusion to the chapter titled ‘The Road Ahead for Tax Stamps’, captures the optimistic tone of this new report from Reconnaissance International. So, it is fair to ask whether the report justifies this optimism, while also asking whether it will satisfy the requirements of its two key target markets: the suppliers and the users of tax stamps.

Suppliers may find the report’s content omits some useful ancillary information, but they should be pleased that it provides a broad base of quantitative data on a market that is otherwise ill-served in this respect, and that it serves well readers from the user market and – more particularly – potential users.

Revenue agencies, meanwhile, will find much to enlighten and guide them in their consideration of whether and how to use tax stamps. And as many of the leading suppliers are supporting the free distribution of this report to revenue agencies around the world, they should be satisfied that it will encourage more of the 100 countries that don’t yet use tax stamps to do so, while also encouraging more of the 91 that do use them to adopt more sophisticated – and therefore more expensive – stamps.

At over 230 pages, this is the most comprehensive and well-presented of Reconnaissance’s three reports on tax stamps, providing an excellent overview of the tax stamp environment, even though it lacks some data one would expect to find here. But it remains the only report on tax stamps, so – along with Reconnaissance’s monthly newsletter and Tax Stamp & Traceability Forum™ – cements the company’s position as the authority and best information source on these small yet advanced examples of security printing.

The report is divided into four sections comprising 18 chapters plus three appendices, and its strength lies in the overview, narrative chapters and country reports. The first two sections, titled ‘Landscape, Drivers and Evolution’ (four chapters, 32 pages) and ‘Implementation and Technologies’ (five chapters, 54 pages), serve as a manual for revenue agencies or other organisations involved in the specification and issuance of tax stamps. Of course, they also provide valuable information to suppliers, helping them marshal arguments to present to potential customers.

The first section establishes a strong case for the use of tax stamps, presenting both information on their successes in combating tax fraud and looking ahead to the likely impact of multilateral regulations.

Highlights include sub-section 2.5 on ‘Proven Success’ in Chapter 2, which summarises detailed information given elsewhere in the report, showing that stamps are most effective when ‘integrated with other control mechanisms’, showing what this means for supply chain control, tracking and tracing and enhanced enforcement. This short section also gives examples of increased tax revenues and reductions in illicit products on the market in six countries, a small selection of data from the later chapters describing tax stamp programmes country by country.

Having established the case for using tax stamps, Section II runs through how this is done, in concise yet comprehensive fashion.

Chapter 6: ‘Practical Considerations of Implementing a Tax Stamp and Traceability System’, contributed by Michael Eads and Ziyaad Butler of Sovereign Border Solutions, sets out guidance for an agency that has decided to introduce a tax stamp system (having been persuaded by Section I!).

As project leader for ISO 22382, I must declare an interest, given that sub-section 6.1, ‘Where to Begin’, draws heavily on that international standard (which is also referenced many times elsewhere in the report), but that title illustrates how this chapter works through from a basic starting point to the design of stamps, their implementation and subsequent monitoring.

Following this management guidance, the report gets into the nitty gritty, explaining the different types of supplier (listing almost 100 of them) and then describing the numerous components and features that make up tax stamps (Chapter 8), the role and methods of serialisation and track and trace (Chapter 9) and formats and application methods (Chapter 10).

These three chapters, contributed by Richard Jotcham of Axess Technologies, give an admirable description of the what, why and how of these various components and processes. Chapter 8 opens with an introduction to the four levels of the security hierarchy and the functional purpose of components, leading into detailed descriptions of key components, grouped under sub-sections covering substrate, security printing processes, applied security features, direct tax marking and authentication devices (ie. for reading or examining security features).

I do have one quibble over the grouping in this chapter. 8.3 ‘looks at technologies other than printed features’, then immediately, in 8.3.1, describes security inks, which is confusing given that they are used to produce those printed features.

There are no details in the first three sections on the cost of tax stamps. It would be helpful to revenue agencies to have included an indication of the cost of buying, issuing and monitoring tax stamps. There are references to relative costs of different types of security feature and printing technique, but no range of actual prices is given. In fact, the introduction to Chapter 8 includes the statement that ‘the cost of production and processing needs to be minimised’, which would have been better stated as ‘the cost needs to be viewed in relation to the increased tax receipts and improved public safety (by reducing illicit goods)’. Admittedly, costs and benefits are given in some of the country descriptions, but it would have been helpful to collate this information in this section.

At this point, it’s appropriate to mention the style and layout of this third tax stamp report. It is not a book to read from cover to cover, from beginning to end, but to dip into when you have decided what information you want. Each chapter contains sub-sections which range from barely a quarter of a page to several pages, as appropriate to the sectional topic. The layout, though, makes this easy to follow, with a consistent and attractive use of shading, different size columns and boxed examples or detailed explanations.

The graphics are also a genuine enhancement to the information; they include photographic examples of tax stamps, security features and equipment, diagrams and – of course – charts and tables, mostly referenced in the text. A minor criticism is that there are some graphics, such as photos of retail displays, which are not captioned, presumably included for tax stamp context.

Dipping in to read specific information would be aided if there were an index, but using the PDF version it is easy to hunt for particular topics.

Nonetheless, a full read will be rewarding as one progresses through the logical sequence of sections (although any one reader might be selective in choosing which country descriptions to read).

Section III, ‘Tax Stamps in Practice’, opens with an overview chapter titled ‘The Global Use of Tax Stamps and Traceability Systems’, followed by descriptions of tax stamp systems in most of the 91 countries that use them.

The estimate is that the use of tax stamps on cigarettes and spirits declined by 12.9% from 2010 to 2018, from 135.4 billion to 117.9, with a flatline forecast for 2023. These figures are extrapolated from data on tobacco and drinks consumption, they are not sourced from producers or users, so it is important to remember they are estimates, albeit fairly accurate ones.

However, 118 billion is not the full story, as the text acknowledges. Sub-section 11.2, ‘Total Tax Stamp Market’, refers back to Chapter 4, ‘The Evolution of Tax Stamps and their Extension to New Market Sectors’, which describes the way that tax stamps are being used on products in addition to their ‘traditional’ use on excisable tobacco and alcohol products.

As shown in Fig 2, these include soft drinks (including packaged water), cannabis and fuels, as well as tobacco substitutes, while the expansion of stamp function is also a growth driver. Though there are extended descriptions and analysis of these new stamp applications in Chapter 4, there is no estimate of stamp quantities for these new areas – something perhaps that could be addressed in a future report when these markets are more established.

The weight given to the descriptions of the countries that use tax stamps can be gauged from the fact that they occupy 70 pages of the report. These are organised by continent, each introduced with an overview.

The depth of description and analysis ranges from a few lines, mainly for small countries where little information is available, to several pages.

There are, for example, several pages about the USA and Russia, not only because these are big countries with large populations, but to describe the developments in those countries.

So, the report examines the implications of each US state being responsible for product taxation and the emerging use of stamps to monitor production and distribution of cannabis, while in Russia there are detailed descriptions of the EGAIS (Unified State Automated Information System) used to track production of all alcohol products and the fur products’ tracking system used in the Eurasian Economic Union (EAEU).

Most usefully and encouragingly, several of the country descriptions include data on the increased tax income and reduction in illicit goods experienced after the introduction of tax stamps, in some cases showing doubling or more of tax receipts and swingeing reductions in illicit goods. This is the data that will encourage other countries to adopt tax stamps.

The quote that opens this review concludes the narrative part of this report, Chapter 18, titled ‘The Road Ahead for Tax Stamps’. This chapter revisits the positive impact expected from the WHO’s Framework Convention on Tobacco Control and other international regulations, reminds readers of the extension of tax stamp programmes to other goods and reviews the impact of technologies.

And so to the appendices: 26 pages of country-by-country tables of recent and forecast consumption of tobacco products and alcoholic drinks (from Global Data), but with tax stamp quantities only for tobacco and spirits. Appendix B sets out the International Tax Stamp Association’s blueprint for the use of stamps to meet the FCTC Protocol’s requirements for tracking and tracing tobacco products, while Appendix C is an excellent, comprehensive, illustrated glossary of relevant terms.

In conclusion, this is an informative report on tax stamps today. Its narrative chapters are generally excellent (subject to the caveats above), but it would have been helpful to have more quantitative data on stamp prices and, for those new markets and applications, numbers as well.

And while it helpfully explains and encourages the use of track and trace systems on tax stamps, predominantly those for tobacco and alcohol, it does not cover any other use of such systems. As these are now mandated for use on pharmaceuticals in many countries and are also used for supply chain control this means the report covers only a small part of this traceability landscape. Perhaps therein lies the opportunity for a further report specifically on traceability.

Tax Stamps and Traceability; pub Reconnaissance International, ISBN 978-1-9163806-1-5